Resources & Tax Updates

IRS Login - Individuals

Securely access your federal tax records, view notices, and manage your IRS account online.

Access IRS Online Account:

➡️ Sign in or create an account

https://www.irs.gov/payments/your-online-account

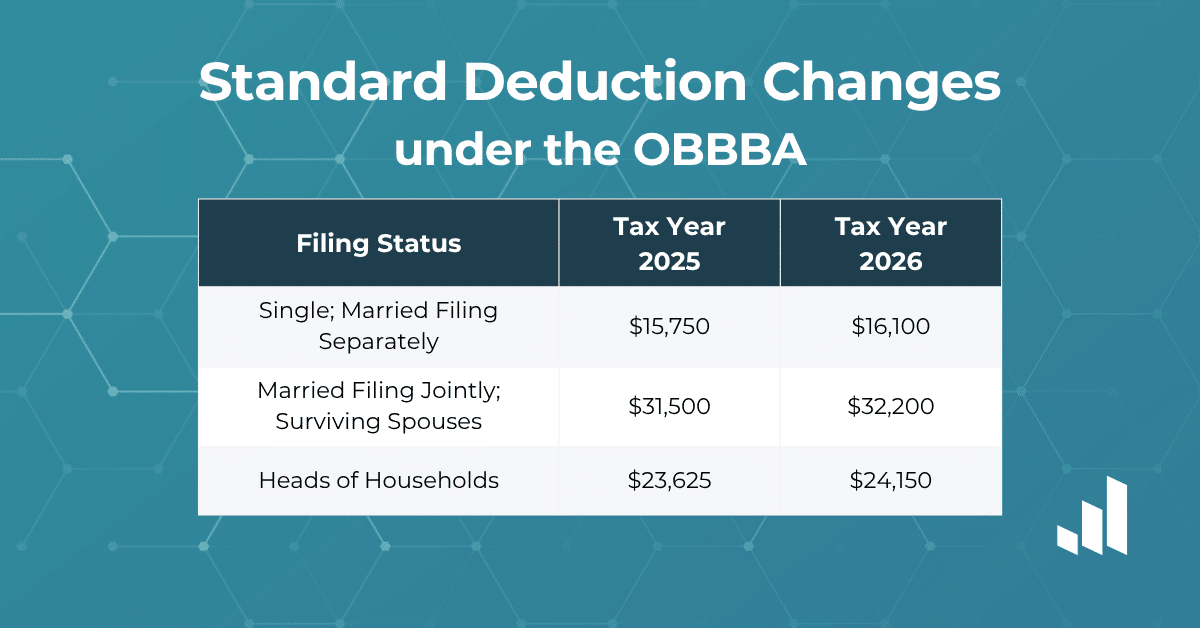

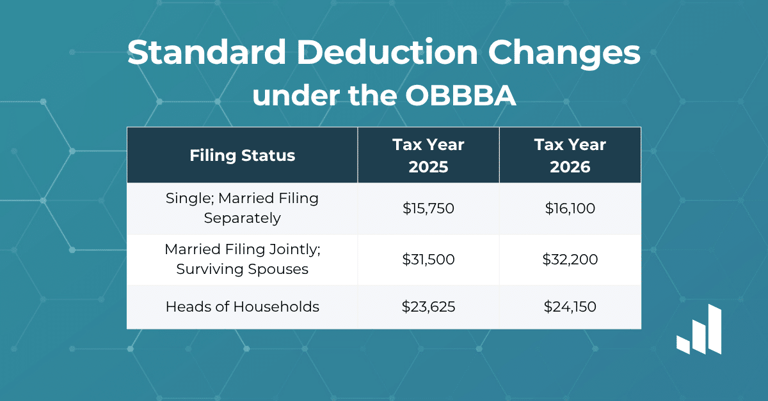

📌 Standard Deduction (Most W-2 Earners)

2025 standard deduction amounts:

• Single or Married Filing Separately: $15,750

• Married Filing Jointly: $31,500

• Head of Household: $23,625

📌 New Above-the-Line Deductions (2025–2028)

Two major new deductions introduced by the One, Big, Beautiful Bill Act are especially relevant to W-2 employees:

🧾 Qualified Tips Deduction

• Employees who receive tips may deduct up to $25,000 of qualified tips from taxable income.

• This applies even if you claim the standard deduction.

• The deduction phases out at higher income levels.

🕒 Qualified Overtime Deduction

• You may deduct up to $12,500 of qualified overtime compensation ($25,000 for married joint filers).

• This is generally the “half-time” portion of overtime pay above regular wages.

These two deductions are new starting with the 2025 tax year (filed in 2026) and apply regardless of whether you itemize.

Itemized Deductions (If You Don’t Take the Standard Amount)

Some W-2 filers may benefit from itemizing if their qualifying deductions exceed the standard deduction:

Common itemized deductions include:

✔ State and local taxes (SALT) — now increased up to $40,000 (limits and phase-outs may apply).

✔ Home mortgage interest on qualified mortgage debt.

✔ Charitable donations (specific limits apply)

✔ Medical & dental expenses exceeding 7.5% of AGI (if itemizing).

✔ Deductible automobile loan interest (up to $10,000 annually for qualifying U.S.-assembled vehicles).

Note: Miscellaneous itemized deductions — such as unreimbursed employee business expenses — remain not deductible federally for most W-2 employees through 2025.

Other Deductions Worth Considering

While not specific to W-2 wages, these can reduce taxable income if you qualify:

🧑🎓 Retirement Contributions

• Traditional IRA or employer-sponsored plan contributions may reduce taxable income (limits apply).

🩺 Health Savings Account (HSA) Contributions

• If eligible, HSA contributions are deductible and can reduce AGI (subject to limits).

👶 Credits (Not Deductions but Tax Reductions)

• Child Tax Credit, Earned Income Tax Credit, education credits, etc., also directly reduce tax liability.

Key Things W-2 Earners Can’t Deduct (Generally)

• Unreimbursed employee business expenses (e.g., home office, tools, travel) are not deductible federally for most employees in 2025.

• Home office deduction is not available for W-2 employees unless self-employed.

• Job search expenses and similar miscellaneous deductions remain disallowed.

Strategic Planning Tips for W-2 Earners

✔ Review whether itemizing yields more benefit than the increased standard deduction.

✔ Track qualified tips and overtime carefully if eligible for the new deductions.

✔ Maximize retirement and HSA contributions to reduce AGI and tax.

✔ Consider state-specific deductions and credits that may differ from federal rules.

Key tax deductions W-2 earners can consider for tax year 2025 (returns filed in 2026) — including new provisions from recent federal tax law changes

📌 100% Bonus Depreciation

Small businesses can now fully deduct the cost of qualified property (equipment, machinery, etc.) in the year it’s placed in service — and this provision has been made permanent under the new law.

📌 Expanded Section 179 Expensing

The amount small businesses can immediately expense under Section 179 rises significantly (e.g., up to ~$2.5 M, with higher phase-out thresholds), encouraging investment in capital assets.

📌 Qualified Business Income (QBI) Deduction Retained

The popular 20% pass-through deduction for eligible small businesses (sole proprietorships, partnerships, S-corps, LLCs) is now permanent, providing long-term stability for planning.

📌 Enhanced R&D Expense Treatment

Domestic research and experimental expenditures can now often be fully expensed in the year paid or incurred, reversing previous amortization requirements and boosting innovation incentives.

📌 Qualified Small Business Stock (QSBS) Gains

The law expanded and improved the tax exclusion on gains from QSBS for qualifying small businesses and investors, including higher caps and more favorable rules, which can help with capital raising and exits.

📌 Family & Employee-Related Credits

Employer credits such as the childcare credit have been significantly increased and enhanced for eligible small businesses, helping with workforce costs.

Key Small Business Tax Changes

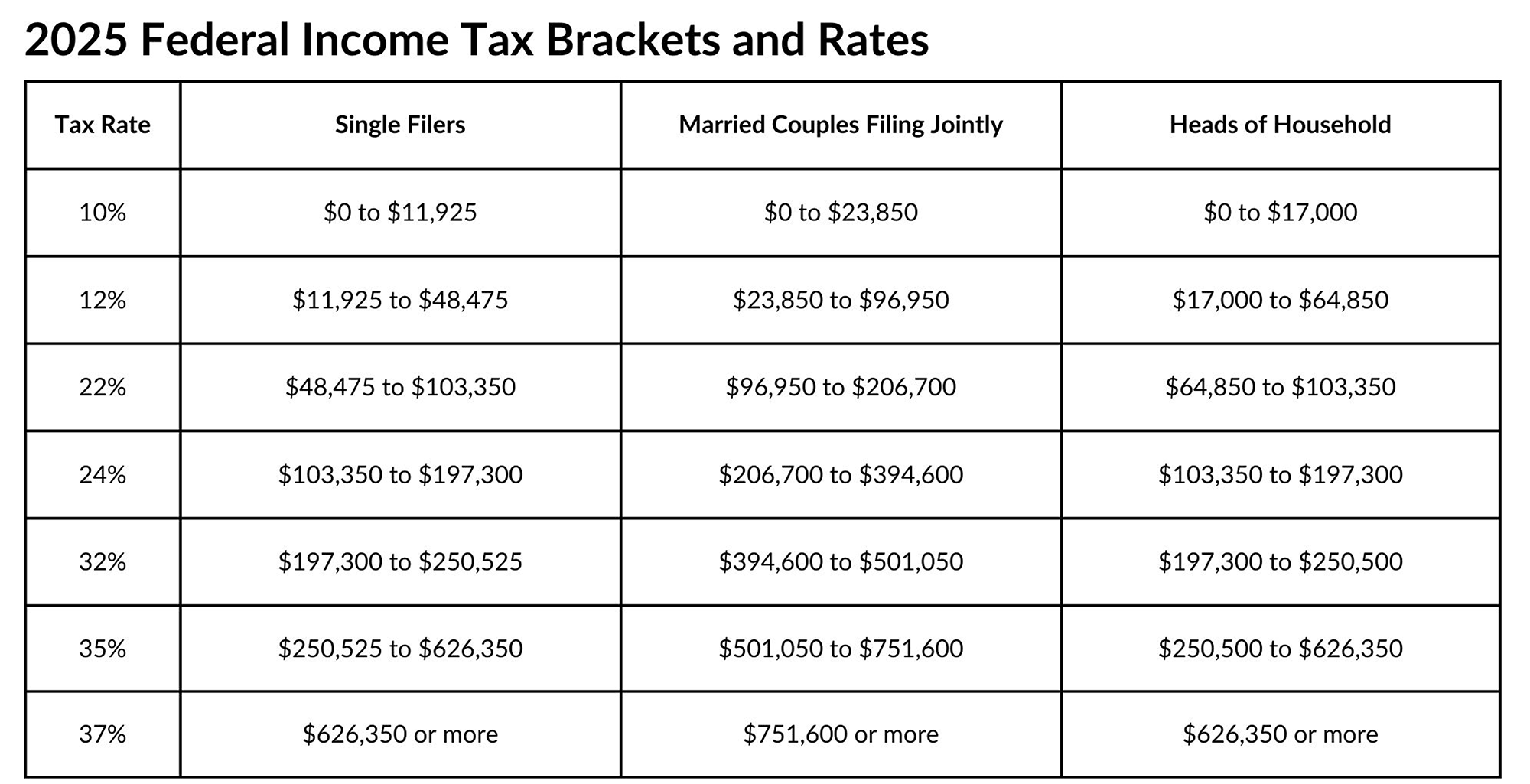

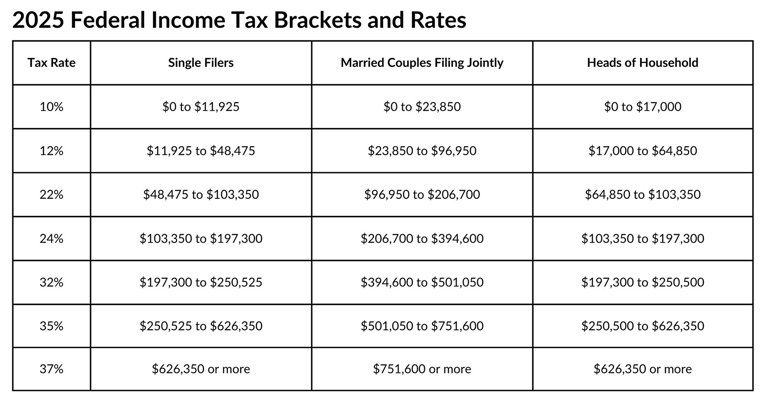

Key Individual Tax Changes

2025 Tax Update — What You Need to Know

Notable changes under the One, Big, Beautiful Bill (OBBB)

Standard Deduction

For tax year 2026, the standard deduction increases to $32,200 for married couples filing jointly. For single taxpayers and married individuals filing separately, the standard deduction rises to $16,100 for tax year 2026, and for heads of households, the standard deduction will be $24,150.

2026 Tax Update — What You Need to Know

Notable changes under the One, Big, Beautiful Bill (OBBB)

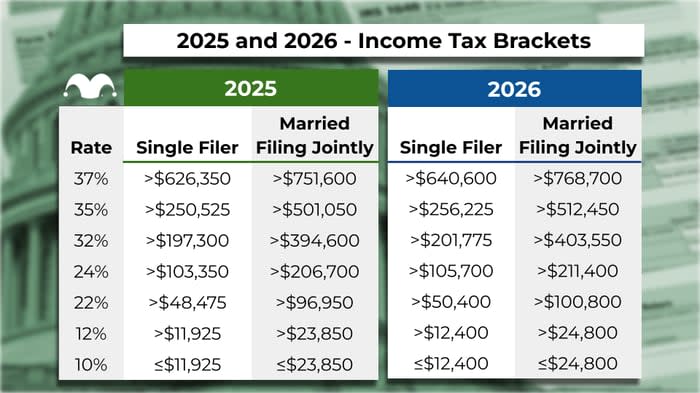

For tax year 2026, the top tax rate remains 37% for individual single taxpayers with incomes greater than $640,600 ($768,700 for married couples filing jointly).

The lowest rate is 10% for incomes of single individuals with incomes of $12,400 or less ($24,800 for married couples filing jointly).

Tax Year 2026 Marginal Rates

Alternative Minimum Tax Exemption Amounts

For tax year 2026, the exemption amount for unmarried individuals is $90,100 and begins to phase out at $500,000 ($140,200 for married couples filing jointly for whom the exemption begins to phase out at $1,000,000).

Estate Tax Credits

Estates of decedents who die during 2026 have a basic exclusion amount of $15,000,000, up from a total of $13,990,000 for estates of decedents who died in 2025.

Adoption Credits

The maximum credit allowed for adoptions for tax year 2026 is the amount of qualified adoption expenses up to $17,670, up from $17,280 for 2025. For tax year 2026, the amount of credit that may be refundable is $5,120.

Employer-Provided Childcare Tax Credit

For tax year 2026, the OBBB significantly enhances an important credit for employers; it increases the maximum amount of employer-provided childcare tax credit from $150,000 to $500,000 ($600,000 if the employer is an eligible small business).